Personal Holiday Loans: How They Work, What to Check, and Alternatives

Personal holiday loans are personal loans used to cover seasonal expenses such as travel, family gatherings, gift purchases, urgent household costs, or other holiday-related needs. Some borrowers also consider quick personal loans when they need access to funds for unexpected expenses during busy holiday periods.

While personal holiday loans may provide a lump sum with scheduled repayment, they also create a financial obligation that extends beyond the holiday season. Alternatives such as using emergency savings, adjusting holiday spending plans, negotiating payment arrangements, or seeking assistance programs may help reduce the need to borrow. Taking time to compare available options can help borrowers make a more informed financial decision.

For borrowers who decide that a loan is appropriate for their situation, installment loan options such as CreditCube may be available to eligible applicants. Loan availability, costs, terms, and approval decisions depend on eligibility, state availability, verification requirements, and the final loan agreement.

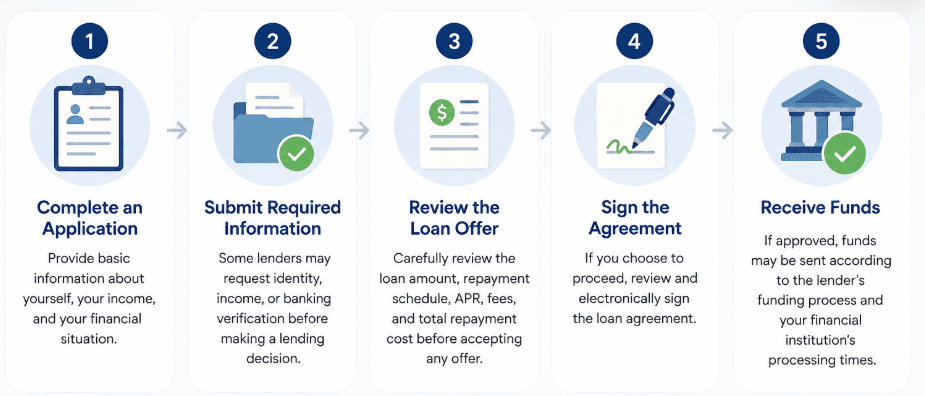

How to Get a Personal Holiday Loan

If you decide that borrowing is the right option for your situation, the application process is often completed online. CreditCube’s process is simple and includes the following steps:

APR and total cost vary by state and borrower eligibility and may be significantly higher than other forms of credit.

What Can Personal Holiday Loans Be Used For?

Personal holiday loans are often used to cover seasonal expenses that arise at the end of the year or during major holidays. The appropriate use of any loan depends on your financial situation, the necessity of the expense, and your ability to repay according to the loan agreement.

Common examples may include:

- Emergency travel

- Higher seasonal utility or heating bills

- Necessary car repairs before planned travel

- Essential household expenses

- Temporary gaps between income and seasonal bills

Some people also borrow for holiday purchases. But borrowing for non-essential spending can create pressure after the season. Can the cost wait? Can you reduce it? Can you cover it another way? If so, compare your options before you borrow.

Ask yourself a few things before you apply. Is the cost needed? Does the payment fit your budget? Could savings, a payment plan, or less spending meet the need instead?

Pros and Cons of Personal Holiday Loans

Personal holiday loans can help cover seasonal expenses when other resources are unavailable. For some households, unexpected costs can be difficult to absorb. According to FINRA's National Financial Capability Study, 35% of Americans would likely be unable to come up with $2,000 within 30 days for an unexpected expense.

However, every loan comes with borrowing costs and repayment obligations. Reviewing both the potential benefits and possible risks can help you decide whether borrowing is the right choice for your situation.

| Benefits | Risks |

|---|---|

| Scheduled installment payments may make budgeting easier than a single lump-sum repayment. | Borrowing adds interest, fees, and overall repayment costs. |

| Funds can be used for a variety of seasonal or holiday-related expenses. | Repayment obligations continue after the holiday season ends. |

| Some lenders offer online applications and electronic document signing. | Approval is not guaranteed and depends on eligibility requirements. |

| A loan may help cover unexpected expenses when savings are unavailable. | Missing payments may result in additional fees or negative financial consequences. |

| Fixed payment schedules can provide more predictability when planning future expenses. | Monthly payments may strain your budget if your income changes. |

| Some lenders consider factors beyond traditional credit scores. | Loan costs can be higher than other financing options. |

| Funds may help address urgent needs such as travel, utilities, or essential repairs. | Borrowing for non-essential spending can create financial pressure later. |

| Early repayment may reduce the total borrowing cost with some lenders. | Taking a new loan to repay an existing loan can increase financial stress. |

No loan is the right solution for every situation. If the expense can be postponed, reduced, or covered through savings or a payment arrangement, those options may be worth considering first.

When a Personal Holiday Loan May Make Sense

A vacation option loan is not the right solution for every situation. However, it may be worth considering when the expense is necessary, temporary, and you have a clear plan for repayment.

- The expense is temporary and necessary. Examples may include emergency travel, essential household bills, or necessary repairs.

- You know how the loan will be repaid. Borrowing should be based on a realistic repayment plan rather than future assumptions.

- The payment fits your budget. Monthly payments should be manageable alongside your other financial obligations.

- You have reviewed the total cost. Understanding the full repayment amount, including interest and fees, can help prevent surprises later.

- You have compared lower-cost alternatives. Savings, payment arrangements, or assistance programs may be available and could cost less than borrowing.

- The expense cannot reasonably be delayed. A loan may be more appropriate when the need is time-sensitive and important.

- You are not using the loan for ongoing financial hardship. Loans are generally better suited to short-term needs than long-term financial challenges.

Before borrowing, consider whether the short term personal loan addresses a temporary situation or a broader financial issue. If the problem is ongoing, alternatives beyond borrowing may be worth exploring.

When a Personal Holiday Loan May Not Be the Right Choice

A personal holiday loan can be useful in some situations, but there are times when borrowing may create more financial pressure than it solves. Taking a moment to evaluate the situation can help you avoid repayment challenges later.

- You are already behind on bills. Adding a new payment obligation may make it harder to catch up on existing expenses.

- You are unsure how you will repay the loan. Borrowing without a clear repayment plan can increase financial stress after the holiday season.

- You need the loan for non-essential spending. Gifts, parties, decorations, or other discretionary purchases may not justify the long-term cost of borrowing.

- You would need another loan to repay this one. Using new debt to manage existing debt can lead to a cycle of borrowing that becomes difficult to break.

- You have not checked the total repayment amount. Understanding the full cost, including interest and fees, is an important part of making an informed decision.

- The loan would make January or future bills harder to manage. If the payment would strain your budget after the holidays, it may be worth exploring alternatives first.

- The financial problem is ongoing rather than temporary. A loan may address a short-term need, but it is less likely to solve a long-term financial challenge.

If any of these situations apply, consider reviewing lower-cost alternatives before borrowing. Savings, payment arrangements, budgeting adjustments, or financial assistance programs may be more appropriate depending on your circumstances.

Alternatives to Personal Holiday Loans

Before applying for a personal holiday loan, it is worth exploring alternatives that may help cover seasonal expenses with less borrowing or no borrowing at all. The right option depends on your financial situation, the urgency of the expense, and your ability to repay.

- Holiday budget adjustment. Reducing spending on gifts, travel, decorations, or entertainment may help lower the amount of money needed during the holiday season.

- Payment plans. Some utility providers, repair shops, medical providers, and other service providers may offer payment arrangements that spread costs over time.

- Emergency savings. Using savings may be a practical option if it helps avoid new debt and does not create another urgent financial shortfall.

- Employer paycheck advance. Some employers offer early access to earned wages, which may help cover short-term expenses without taking out a loan.

- Credit union small-dollar loan. Some credit unions provide lower-cost borrowing options for eligible members, often with more affordable terms than other forms of credit.

- Credit card. A credit card may work for smaller purchases if the balance can be repaid quickly. However, interest charges can become expensive when balances are carried over time.

- Buy Now, Pay Later (BNPL). BNPL services can split purchases into smaller payments, but missed payments and overspending can create additional financial challenges.

- Nonprofit credit counseling. Credit counseling organizations may help if holiday spending is part of a broader debt or budgeting issue.

Some borrowers still decide a personal loan fits best. For eligible borrowers, CreditCube offers installment loans with set payments. CreditCube offers high-cost installment loans to eligible borrowers. These loans may carry higher APRs than traditional bank products. Before you apply, review the terms, the total cost, the rules, and the alternatives. Then decide if borrowing is right for you.

FAQ - Personal Holiday Loans

What are personal holiday loans?

Personal holiday loans are personal loans for seasonal costs. They may cover some holiday costs. But compare the total cost, the terms, and the alternatives before you apply.

Are personal holiday loans the same as payday loans?

No. Payday loans are often short-term loans that require repayment in a single lump sum. Personal holiday loans are typically installment-style personal loans repaid through scheduled payments over time. Terms, costs, and repayment structures vary by lender and loan agreement.

Can I use personal loans for holiday gifts?

Some personal loans may be used for holiday gifts or other seasonal purchases. However, borrowing for non-essential spending can create repayment pressure after the holiday season. Before borrowing, consider reducing expenses or exploring alternatives that do not require new debt.

Are personal holiday loans a good idea?

Personal holiday loans may be an option when the expense is necessary, temporary, and repayment fits comfortably within your budget. Personal holiday loans may not be a good fit if you are already struggling with debt, unsure how you will repay, or borrowing for spending that can be avoided or delayed.

What should I check before applying for a personal holiday loan?

Review the APR, the total cost, the fees, and the schedule. Check the state availability, the lender rules, and the missed-payment results. Make sure the payments fit your budget.

What are alternatives to personal holiday loans?

Options include adjusting your holiday budget, asking for payment plans, and using savings. You could also seek an employer paycheck advance, a credit union small-dollar loan, or a credit card used with care. Buy Now, Pay Later services and nonprofit credit counseling are options too.

Recent Articles

Medical Loans for Bad Credit: Fast Help for Bills

Medical loans for bad credit explained. Learn how they work, who qualifies, ...Loan With 500 Credit Score: Approval Options

Loan with 500 credit score options explained. Learn how to qualify faster, w...Same Day Loan Funding Explained | ACH vs Wire Transfers

Same day loan funding explained. Learn how ACH, wire transfers, and bank pro...Home Improvement Loans With Bad Credit: 2026 Guide

Home improvement loans with bad credit explained. Learn options, rates, and ...AI Loan Approval Is Faster and You’ll Be Shocked How!

Discover how AI loan approval and automated underwriting are revolutionizing...Graduates HATE This: New Student Loan Hacks for 2025 Revealed!

Explore powerful student loan strategies, repayment hacks, and student loan ...Get your money today

Apply for a loan NOW!

Applying does NOT affect your FICO® Score!

Have questions?

Please call us by phone:

Credit Cube © 2026. All rights reserved

CreditCube is a Tribal enterprise, wholly owned and operated by the Big Valley Band of Pomo Indians, a federally-recognized American Indian tribe and sovereign government. Any Agreement entered into as a result of this Application shall be governed by applicable Tribal and federal law. Each aspect of communication and transaction with/on this site will be deemed to have occurred in CreditCube’s Big Valley Band of Pomo Indian Reservation offices, regardless of the location where you are accessing or viewing this site.

⚠ Please note: This is an expensive form of borrowing. CreditCube loans are designed to assist you in meeting your short-term borrowing needs and are not intended to be a long-term financial solution! Examples of emergency reasons why these loans might be used include unexpected emergencies, car repair bills, medical care, or essential travel expenses.

* Loan approvals are subject to underwriting. Approval may take longer if additional verification documents are requested. Not all loan requests are approved. CreditCube reviews your information in real-time to determine whether your information meets our lending criteria. You acknowledge that by completing and submitting the website application that you are applying for a Loan. We verify applicant information through national databases including, but not limited to, Clarity Services, Inc., a credit reporting agency, and we may pull your credit in order to determine your eligibility and ability to repay.

** Maximum loan amount is $500 for first-time customers. For returning CreditCube customers, rates may go down over time based on your CreditCube Loyalty Program status and your payment history with us. Please see our Loyalty Program page for more information.

*** Loan Applications processed and approved before 3pm EST Monday-Friday are typically funded on the next business day. Example: If your loan is processed and approved on Friday before 3pm EST, the loan will typically be funded on the following Monday. Deposit times may vary depending on your bank. Business Day means Monday through Friday excluding all federal banking holidays.

CreditCube does not lend to residents of Pennsylvania, Connecticut, Minnesota, New York, Vermont, Virginia, West Virginia, Illinois and Georgia. Availability of installment loans in your state is subject to change at any time with or without notice at the sole discretion of CreditCube.